From around 2010 to 2013 I ran a small volunteer organization called Geoburst. Geoburst.ca continued to function for a long time afterward and now it’s time to take it down. Find Geoburst’s “About” page below.

Geoburst.ca's Banner

About Geoburst

The problem with mathematics

Dozens of books have been written about math education, and not in error, but GeoBurst’s philosophy can be summarized in a single sentence. We must teach that mathematics has intrinsic value, for being beautiful, fun, surprising, and expansive.

When kids practice their multiplication tables, we think of this as a pianist practicing scales. When the pianist is ready, however, he or she plays beautiful music. That is why we help kids take a break from their multiplication tables, to remind them of what beautiful mathematics they are preparing for.

GeoBurst’s Mission

GeoBurst mission is to Create Zest for Mathematics. By sharing our love for this subject, we hope to spread an enthusiasm for mathematics that will shine a positive light on a challenging subject for all of us.

By seeding positive early experiences with mathematics, GeoBurst’s activities can soothe the tension that some students feel about mathematics, encourage kids to pursue science and engineering, and ultimately increase the amount of beautiful mathematics that Canadians do.

GeoBurst’s Vision

We want every school in British Columbia to be equipped with a clearly labelled treasure chest of fun mathematical activities, and every student to experience at least two special presentations on mathematics by the time they finish grade 7. In the interest of creating equal opportunities, we are donor funded, and provide our services free of charge whenever possible.

GeoBurst

Math Catcher

Mathematics through aboriginal story telling

We work closely with Math Catcher through consulting and the integration of our interactive shows into their program. This partnership benefits our programs mutually, and has helped GeoBurst develop its mission and activities by providing a raison-d’être and an audience at an early stage in our development.

GeoBurst is proud to work closely with award winning math professor, Dr. Veselin Jungic, and First Nations role models to bring a much needed enhancement to mathematics education for remotely located and urban Aboriginal students. GeoBurst is an integral part of their school visiting program, and Math Catcher’s influence and contributions continue to be indispensable to the formation of our values, and the operation of our program.

My main sheet and vang used to connect to a simple eye near the base of the mast until one day the threads gave way and it popped out.

Broken Main Sheet and Vang Eye

Whether it was my fault or not I don’t know, since I didn’t see it happen, but now that I have to fix it I’d like to make it and the halyard organizer more robust, by replacing them both with a mast-base organizer plate. I envision something like the plate pictured below, but without the hinge.

Halyard organizer plate (hinged)

From the picture of my own mast base, it looks like I already have some sort of aluminum casting at the foot of my mast, so if I unstep the mast and successfully remove the casting, I should be able to slip a plate underneath it… Let’s hope I can get it off!

I’ll update this post as the project moves forward.

There is a place in English Bay, near Vancouver, called Point Atkinson, which is notorious for causing engine troubles. The guy from C-Tow joked that it was something of a local Bermuda triangle. He said that to me after towing me to my slip at Lynnwood for around $400 CAD and added, “One time at Point Atkinson I changed my own fuel filter 3 times.”

The Saltire in False Creek.

My engine had failed there too, shortly before getting towed, while I was sailing single-handedly. After thinking about what the tow-dude said I read up on cleaning and maintaining fuel and decided to not only change the fuel filters, but to also polish the fuel using the existing water separator.

I disconnected the Racor 215 series water separator from The Saltire’s fuel lines and screwed in 5/16th hose diameter connectors. I connected the intake to a fuel-line hose and a matching metal tube made of automotive brake-line for vacuuming inside the tank. I connected the exit to a Mr Gasket 12V diesel fuel pump, purchased for $60 CAD at an automotive parts supplier; I have supplied a link to it but any such pump will do the job. Part of the time I had a prefilter before the water separator but eventually it clogged up and I removed it.

Existing primary filter setup.

Fuel gauge float port.

Initially I tried to polish using the existing Racor R15T 10 micron filter, but it was so clogged with gunk that no fuel would pump through. That pretty much explains the issue I had on the water, and I will be carrying a spare Racor from now on!

Pumping about 110L of fuel out into jerry cans and back into the tank took about 4 hours. The pump is rated to move it faster than that, but various things slowed me down.

Rusty fuel filter.

Dirty fuel filter.

I separated about 600mL (over a pint!) of water from the fuel, and the tank looked pretty clean on the inside afterwards.

600ml water from fuel.

A quick tour of my fuel polishing system

This year I set out to learn about investing and trading on the stock market. I signed up for a practice account on Questrade which comes with a healthy supply of fake cash and started making pretend trades. Pretty soon I realized that I needed a written comprehensive plan, complete with a strategy and specific shares that I want in my portfolio. Google spreadsheets to the rescue!

I found a spreadsheet that serves as a starting point on Dough Roller and added support for multiple accounts and account types.

Here is a direct link to the spreadsheet

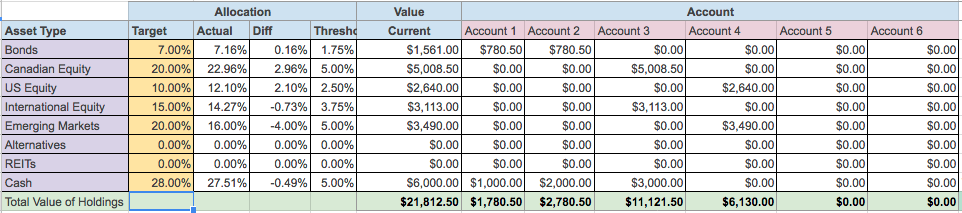

The spreadsheet provides a summary of your holdings by account type and asset type, where you can also view the difference between your portfolio allocation and your target allocation.

Account Balances by Asset Type.

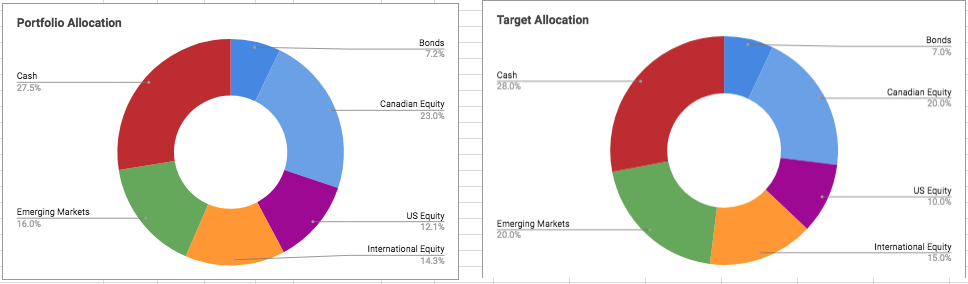

Below the account summary there is also a visual representation of your target and actual allocations.

Porfolio Target and Actual Allocation.

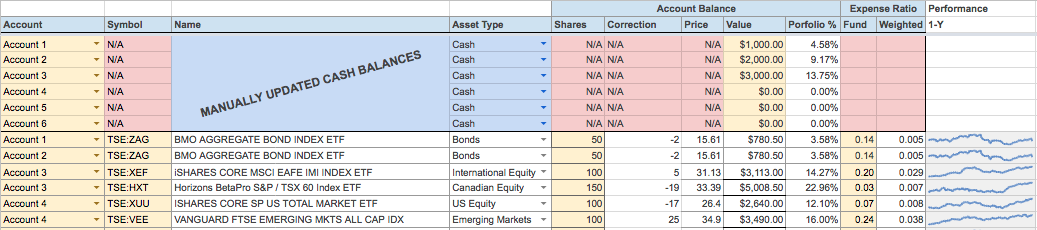

Actual holdings are specified on the holdings page by giving a ticker symbol and number of shares owned.

Portfolio Share Holdings.

Anything and everything in my blog post could be factually incorrect. Please verify any information you get here with other, more reliable sources and check my math. If you see a problem please let me know in the comments.

Enjoy!

Canada offers a registered account to incentivise people to invest in their childrens’ education. It’s a bit complicated and most blogs and news articles I found only offer this very basic advice: “take advantage of the free money”. It’s not that bloody simple though.

Anything and everything in my blog post could be factually incorrect. Please verify any information you get here with other, more reliable sources. If you see a problem please let me know in the comments.

At a basic level the RESP works as follows: You incrementally add after-tax money to an account, to a maximum of $50,000.00, and the Government matches your yearly contributions with 20% each year, to a maximum of $7,200.00. You invest this money aggressively early on, and less aggressively later, while it is sheltered from taxes. When the beneficiary, usually your child, attends a post-secondary they can receive money from the gains made by the investment, as well as from the grant itself, and pay tax on the money as if it were the beneficiary’s income.

The details, provided by the Canada Revenue Agency, get complicated though, which makes it hard to answer a number of questions without breaking out the spreadsheets.

- How big will the investment be, after tax, if the beneficiary does not use the money?

- If you have $50,000 when you open the account, should you dump it all into the RESP, or take advantage of the grant and make several payments over several years?

These questions pertain to how the money is paid out, so let me define those ways. An EAP is a payment from the gains on the whole investment (grants and gains) made to the beneficiary who is enrolled in a qualifying educational program. EAPs are taxed as the beneficiary’s income.

An AIP is a payment from the gains on the contributions to the subscribers (who originally made the contributions). Grant money cannot be paid to the subscribers, and it is lost if the beneficiary does not use it. The original contributions were made by subscribers with after-tax money, so they are paid out without additional taxation. AIPs are taxed as the subscriber’s income plus 20% (12% in Quebec).

Obviously there could be a significant difference in taxation between EAPs and AIPs, so you need to consider the chance that AIPs will be paid out instead of EAPs, and how much that will cost you. An additional, hidden cost, is that in a normal taxable account, capital gains and dividends are taxed at a lower rate than regular income. Let me illustrate this with a simplified example.

Let’s say you invest $10,000.00 for 10 years and it grows to $15,000.00. You sell the investment in year 10 and declare $5000.00 in capital gains. Suppose further that your combined federal and provincial income tax marginal rate is 32% and your capital gains are taxed at 16%. Your beneficiary’s income tax marginal rate is 21%.

- If the $5,000.00 gains are paid as EAPs, the beneficiary pays $1,050.00 in tax.

- If the $5,000.00 gains are paid as AIPs, the subscriber pays $2,600.00 in tax.

- If the $5,000.00 gains are paid as capital gains, the account holder pays $800.00.

The 20% penalty against AIPs is huge, of course, but the difference between investing in a taxable account and getting EAPs is more subtle. Many investments pay dividends, which are taxed a bit more heavily than the capital gains mentioned in (3), plus the RESP account in (1) may have accumulated some additional grant money. Let’s consider that situation. Suppose the RESP also earned the full 20% grant on the $10,000.00 in contributions, and that the investment included some dividends that were taxed at 25%. Again, we are simplifying things.

- There are $5,000.00 gains and $2,000.00 in grants to be paid as EAPs. The beneficiary receives $5,530.00 and pays $1,470.00 in tax.

- If the $5,000.00 gains are paid as AIPs, the subscriber receives $2,400.00 and pays $2,600.00 in tax.

- If the $4,000.00 gains are paid as capital gains and $1,000.00 are paid as dividends, the account holder receives $4,120.00 and pays $880.00 in tax.

As expected, the AIP payments remain the same, but the EAPs now yield a 34% improvement on the gains in a normal taxable account. Of course, this is still a bit too simple. Firstly, the $10,000 cannot be contributed to the RESP all at once if the $2,000.00 in grants are to be obtained. That means that for some of the time, that original $10,000.00 sits in a taxable account. Secondly, only up to $36,000.00 of the RESP benefits from a 20% grant, because of the $7,200.00 limit on the total grant, so we can’t apply the same logic to a $50,000.00 RESP account.

We’ll need a spreadsheet to finish this

We are considering four ways of investing $50,000.00.

- Contribute the $50,000.00 to the RESP and get a $500.00 grant.

- Split the $50,000.00 over the RESP and a taxable account, and gradually move the money to the RESP to maximize the $7,200.00 grant.

- Put the $50,000.00 in a taxable account.

- Maximize the grant, but keep the remaining money in the taxable account.

And we are considering three ways the investment growth and grants can be taxed.

- Grants and investment growth are paid out as EAPs, taxed as the beneficiary’s income.

- Grants are lost, but investment growth is paid out as AIPs (after the beneficiary turns 21), taxed as the subscriber’s income.

- There are no grants, and the investments can be paid out any time, taxed as investment growth (capital gains, dividends, interest, etc).

We don’t know in advance whether we’ll have EAPs and not AIPs, so we factor the likelihood into our assumptions. We need to make a bunch of assumptions, in fact so let’s make them.

Assumptions:

- 6% growth (mostly stocks) for 10 years, then tapering off to 3% (mostly bonds) for the final years.

- The money is tallied when the child is 21, the earliest year AIPs can be paid. Realistically the EAPs will be paid earlier.

- The subscriber’s family income is over 90k (if not, the grant gets paid a bit more aggressively).

- Subscriber marginal rate is 32%.

- Beneficiary marginal rate is 21%.

- Avg investment tax is 20%.

- Likelihood that EAPs are NOT needed is 20% (child gets scholarships, dies, drops out of school, whatever).

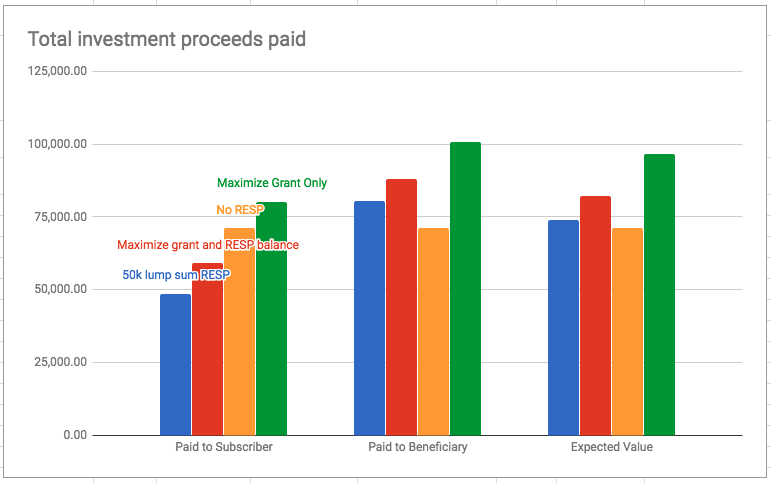

The first eight bars plot the investment proceeds that would be paid out as AIPs, or as EAPs combined with whatever non RESP money exists in each investment method, after tax. The last four bars plot the expected value of the investments based on our assumptions above. The assumptions can be changed in the spreadsheet.

Play around with the spreadsheet here.

RESP Returns by Investment Method.

And the winner is… maximize the grant and keep the rest of your money out of the RESP!

Remarks: The definition of qualifying educational program is fairly broad and inclusive, so if the beneficiary is alive, half-serious about any sort of educational program and doesn’t have a scholarship, they will probably use the grant. Note also that some of the provinces offer an additional grant. For example BC offers another $1,200.00 or so when the Child turns 6.

If you find any mistakes or oversights in my calculations or spreadsheet, please let me know in the comments!

Enjoy (taxes).